Taxation Of Social Security Income

Nov 10, 2019 • Written by Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

Blog Home » Retirement Income » Taxation Of Social Security Income

Most workers are well aware they pay Social Security taxes on their income throughout their career. Both you and your employer each pay a 6.2% Social Security tax on your income, up to the maximum wage base ($137,700 in 2020).

Unfortunately, most workers are unpleasantly surprised to learn they may also pay taxes on a portion of their Social Security benefit income when in retirement.

In fact, according to the Social Security Administration (SSA), approximately 60% of current Social Security recipients pay federal income tax on part of their benefit. Approximately 20% of beneficiaries pay taxes on 85% of their benefit. An increasingly higher number of retirees will be required to pay tax on their Social Security benefits over time because the income thresholds used to determine the taxation are not adjusted for inflation each year.

The History of Taxing Social Security Income

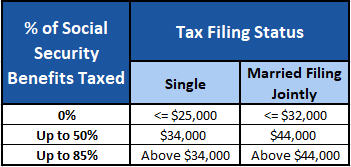

When the Social Security program was created in 1935, the Treasury Department issued specific tax rulings making it clear that Social Security benefits were excluded from federal income taxation. That all changed in 1983 when lawmakers adopted rules requiring Social Security recipients to include some of your Social Security benefits in taxable income if your “combined income” – that is, your adjusted gross income plus tax-exempt bond interest and one-half of their annual Social Security benefits – was higher than $25,000 for single filers, or $32,000 for joint filers.

A decade later, Congress once again took up the issue of Social Security taxation and made its most recent revisions. In 1993, lawmakers added a second set of thresholds above which a greater percentage of Social Security benefits would be subject to tax. Specifically, for single filers making more than $34,000 in combined income, or joint filers making more than $44,000, as much as 85% of Social Security benefits could be subject to tax.

How Social Security is Taxed Today

Social Security benefits become taxable if your combined income exceeds $25,000 as an individual and $32,000 as a married couple. If your income is between $25,000 and $34,000 ($32,000 and $44,000 for couples), income tax will be due on 50% of your Social Security benefit. Retirees with incomes that exceed $34,000 ($44,000 for couples) pay income tax on up to 85% of their Social Security benefit.

A couple of examples to illustrate:

Example 1. Brian and Jennifer have an AGI of $27,000 and receive combined Social Security benefits of $16,000. As a result, their combined income is $27,000 + $8,000 (half of Social Security benefits) = $35,000, which is $3,000 above the $32,000 threshold. This means that 50% x $3,000 = $1,500 of their Social Security benefits are subject to taxation, which ultimately increases their AGI to $27,000 + $1,500 = $28,500.

Example 2. Donald and Sandy have an AGI of $44,000 and receive combined Social Security benefits of $24,000. As a result, their combined income is $44,000 + $12,000 = $56,000, which is $12,000 above the upper $44,000 threshold. This means that $16,200 of benefits are subject to taxation (which is technically 50% of the amount from $32,000 to $44,000 plus 85% of the excess above $44,000), which ultimately increases their AGI to $44,000 + $16,200 = $60,200

As stated previously, the income thresholds for Social Security taxes are not adjusted for inflation each year; the thresholds have remained constant since 1993! As time passes, more and more retirees will be required to pay tax on their Social Security benefits.

State Taxation of Social Security Income

As if paying federal income taxes isn’t bad enough, some Social Security recipients also have to pay state income tax on their retirement benefits. The majority of states (37 of them) do not tax Social Security benefits. Unfortunately, Colorado isn’t one of them!

Colorado allows you to exempt a certain amount of your Social Security benefits from state income tax. You can earn a total of up to $24,000 in Social Security benefits and other types of retirement income without paying any state income tax. Income above that exemption amount will be subject to state tax.

Be Tax-Smart with Social Security

It may come as an unpleasant surprise to many retirees that Social Security benefits can be taxable. But by knowing that in advance, you may be able to create a retirement income plan to minimize federal and state income taxes on your benefits.

While it’s important to understand and account for the taxation of Social Security income, it also should not be overemphasized. It’s most important to understand how Social Security income and taxes fit into your overall comprehensive retirement plan.

Related articles:

Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

Paul Staib, Certified Financial Planner (CFP®), RICP®, is an independent Flat Fee-Only financial planner. Staib Financial Planning, LLC provides comprehensive financial planning, retirement planning, and investment management services to help clients in all financial situations achieve their personal financial goals. Staib Financial Planning, LLC serves clients as a fiduciary and never earns a commission of any kind. Our offices are located in the south Denver metro area, enabling us to conveniently serve clients in Highlands Ranch, Littleton, Lone Tree, Aurora, Parker, Denver Tech Center, Centennial, Castle Pines and surrounding communities. We also offer our services virtually.

Read Next

Your 2018 Tax Fact Sheet

• Written By Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

The turn of the calendar page usually ushers in a few small tax adjustments – allowable 401(k) and IRA contributions…

6 Key Reasons Why Investing in a Taxable Account Is Underrated

• Written By Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

Investors are often schooled in the virtues of stashing money in tax-sheltered savings vehicles, whether IRAs, company retirement plans, 529s,…