The 3 Tax Phases of Retirement Planning: Why Early Retirement Years Offer the Greatest Tax Planning Opportunity

Mar 20, 2026 • Written by Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

Blog Home » Retirement Income » The 3 Tax Phases of Retirement Planning: Why Early Retirement Years Offer the Greatest Tax Planning Opportunity

The 3 Tax Phases of Retirement Planning

Most people assume that their taxes will naturally decline once they retire.

After all, the paycheck stops, income drops, and the assumption is that taxes follow.

In reality, retirement typically unfolds through three distinct tax phases, each with different planning opportunities and risks.

Understanding these phases can dramatically improve how retirees manage their income, investments, and taxes over the course of retirement.

At Staib Financial Planning, we often explain this concept using the framework below.

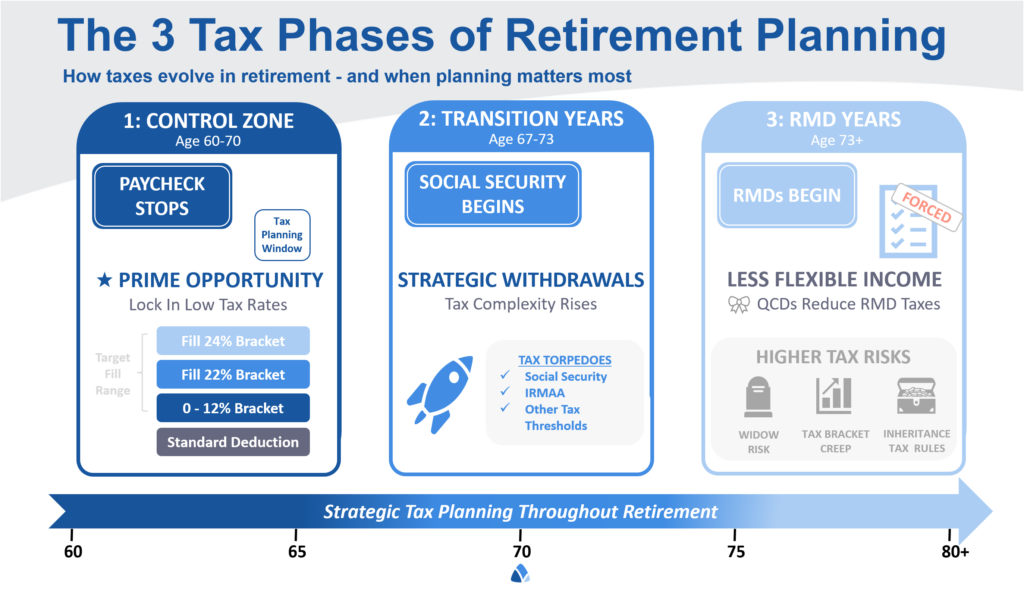

This framework illustrates how taxes evolve throughout retirement – and more importantly, when strategic tax planning matters the most.

Phase 1: The Control Zone (Age 60–70)

The early years of retirement are often the most powerful tax planning window available.

This phase typically begins when:

Your paycheck stops.

At this point, many retirees experience a temporary drop in taxable income because:

- employment income ends

- Social Security has not yet started

- Required Minimum Distributions (RMDs) have not begun

This creates a unique opportunity to intentionally manage taxable income.

Why This Period Matters

During this phase, retirees can often lock in relatively low tax rates by strategically generating income from tax-deferred accounts.

For example, many retirees intentionally “fill up” lower tax brackets such as:

- the 0–12% tax brackets

- the 22% tax bracket

- and sometimes the 24% bracket

This is commonly done through strategies such as Roth conversions, which move money from tax-deferred retirement accounts into Roth accounts while paying taxes at known rates today.

The goal is simple:

Pay taxes strategically when rates are relatively low rather than being forced to later when income may be higher.

Phase 2: Transition Years (Age 67–73)

The second phase typically begins when Social Security benefits start.

At this stage, the tax picture begins to change.

Income now may come from multiple sources:

- Social Security

- retirement account withdrawals

- investment income

- pensions

This can introduce additional layers of tax complexity.

Tax “Torpedoes” Begin to Appear

During this phase, retirees may encounter several tax thresholds that can significantly affect their total tax bill, including:

- Taxation of Social Security benefits

- Medicare IRMAA surcharges

- capital gains thresholds

- other income-based tax triggers

Strategic withdrawal planning becomes critical in this phase to avoid unintentionally pushing income into higher tax brackets or triggering additional taxes.

This is where careful retirement income planning and withdrawal sequencing can help reduce long-term tax costs.

Phase 3: RMD Years (Age 73+)

The third phase begins when Required Minimum Distributions (RMDs) start.

At this point, retirees lose much of the flexibility they had earlier.

The IRS now requires that certain amounts be withdrawn from tax-deferred accounts each year.

These distributions can significantly increase taxable income.

Why Taxes Often Rise Later in Retirement

Several factors can cause taxes to increase in this phase:

- large RMDs from traditional retirement accounts

- Social Security income

- taxable investment income

- loss of certain tax deductions

Additionally, retirees may face several risks during this phase, including:

- the widow’s tax penalty

- tax bracket creep

- higher taxes for inherited retirement accounts

Without earlier planning, these factors can push retirees into higher tax brackets later in life.

Why Early Retirement Planning Matters

One of the most important insights from this framework is that tax flexibility often declines as retirement progresses.

In the early retirement years, retirees often have the most control over their taxable income.

Later in retirement, income becomes more rigid due to:

- Social Security benefits

- RMD requirements

- portfolio withdrawals needed for spending

This is why many tax-efficient retirement strategies focus heavily on the Control Zone years.

Taking advantage of this window can potentially reduce lifetime taxes and create greater flexibility later in retirement.

Common Strategies Used During the Control Zone

During the early retirement years, several strategies may help improve tax efficiency.

These can include:

- Roth conversions

- strategic withdrawals from retirement accounts

- capital gain harvesting

- managing Social Security claiming strategies

- coordinating income with Medicare IRMAA thresholds

Each retiree’s situation is unique, so these strategies should be evaluated carefully within a comprehensive retirement plan.

The Big Picture

Rather than viewing retirement as one long phase, it can be helpful to think of it as three distinct tax environments.

- Control Zone — the years with the most tax planning flexibility

- Transition Years — when tax complexity begins to increase

- RMD Years — when income becomes less flexible

Understanding how these phases interact can help retirees make more informed decisions about:

- retirement withdrawals

- Roth conversions

- Social Security timing

- long-term tax strategy

Ultimately, the goal is not simply to minimize taxes in any one year, but to reduce taxes across the entire retirement lifetime.

Learn More About Tax-Efficient Retirement Planning

If you’re approaching retirement or have recently retired, understanding how these tax phases apply to your situation can be incredibly valuable.

You may also find these related resources helpful:

- 5 Stealth Taxes That Can Impact Your Retirement

- 6 Strategies to Reduce Taxes in Retirement

- Tax Planning Principles

Call to Action

If you’d like help evaluating how these tax phases apply to your retirement plan, you can schedule a conversation here: Schedule a Consultation

Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

Paul Staib, Certified Financial Planner (CFP®), RICP®, is an independent Flat Fee-Only financial planner. Staib Financial Planning, LLC provides comprehensive financial planning, retirement planning, and investment management services to help clients in all financial situations achieve their personal financial goals. Staib Financial Planning, LLC serves clients as a fiduciary and never earns a commission of any kind. Our offices are located in the south Denver metro area, enabling us to conveniently serve clients in Highlands Ranch, Littleton, Lone Tree, Aurora, Parker, Denver Tech Center, Centennial, Castle Pines and surrounding communities. We also offer our services virtually.

Read Next

The Ins and Outs of Social Security Benefits and Taxes

• Written By Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

It’s an unpleasant fact of life: The taxman can take a bite out of your Social Security benefits. The…

8 Behavioral Biases That May Hurt Your Investments

• Written By Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

Do you feel the pain of loss more than the joy of gains? How to separate emotions from investing. It’s…